RUTHERFORD COUNTY, TN - Financial statements of Rutherford County were audited by Tennessee’s Comptroller of the Treasury and released in the Annual Comprehensive Financial Report for the county. Details in the documents reveal two issues in the Assessor of Property Office and one issue in the County Office of Finance. According to the Independent Auditor’s Report that was filed 6-weeks ago by Jason E. Mumpower, Comptroller of the Treasury for Tennessee, the audit focused on the fiscal year that ended on June 30, 2024.

The first audit finding shows that in the Rutherford County Office of Finance, led by Michael Smith, CPA, "expenditures were misclassified in the accounting records of the general fund." According to the comptroller’s findings, multiple expenses were misclassified as reappraisal costs. This misclassification could mislead residents about how funds are actually being utilized. As a result, the county finance office has been instructed to improve its accounting practices. The findings show that management argued that all staff contribute to reappraisals and that their budget practices comply with state regulations.

Smith, the County Finance Director, acknowledged the findings in a memo to Jeff Bailey, a Legislative Audit Manager in the Tennessee Comptroller office. However, Smith did not agree with the findings and therefore, no corrective action plan was submitted.

In the Assessor of Property Office, led by Assessor Rob Mitchell, the comptroller's report indicates that the assessor did not properly prorate improvements and new construction, nor did the office record all improvements in the appropriate tax year. This oversight meant that some homes were not correctly assessed for taxes in the 2023 tax year. The comptroller’s office stated that this happened because change orders weren’t submitted on time, leading to inaccurate property values.

On page 344 of the report, the comptroller found that the assessor did not record all improvements made to properties in the correct tax year. Specifically, it was noted that some changes were deferred until the next reappraisal cycle, set for 2026, which is against state law (Tennessee Code § 67-5-1601). The audit concluded that current practices have likely caused inaccuracies in property assessments. Documents show that Assessor Mitchell agreed with the findings and stated that steps are being taken to improve their processes. In documents submitted to the state, Mitchell said that corrective measures are underway. Mitchell also noted that corrective measures were taken immediately.

The report underscored the need for better management practices in how the office records and handles expenditures, particularly regarding reappraisal funding. Overall, the audit indicated that the Assessor's office needs to enhance its practices in managing property evaluations to comply with state regulations and ensure accurate assessments.

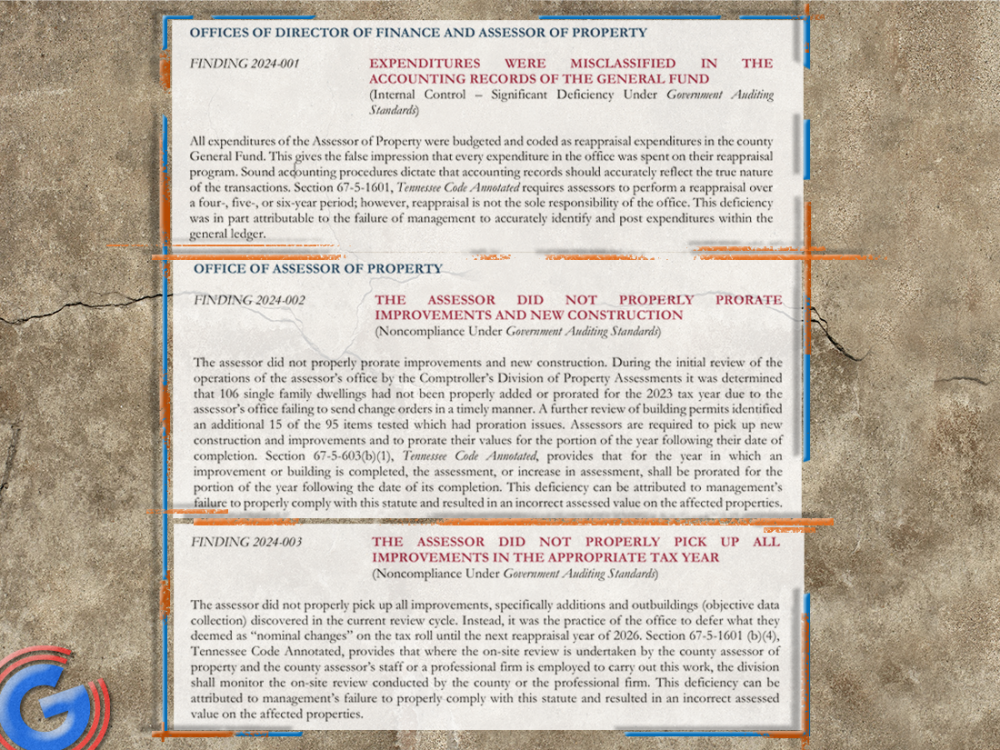

FINDING Number 1: EXPENDITURES WERE MISCLASSIFIED IN THE ACCOUNTING RECORDS OF THE GENERAL FUND - (Internal Control – Significant Deficiency Under Government Auditing Standards) Page 343:

All expenditures of the Assessor of Property were budgeted and coded as reappraisal expenditures in the county General Fund. This gives the false impression that every expenditure in the office was spent on their reappraisal program. Sound accounting procedures dictate that accounting records should accurately reflect the true nature of the transactions. Section 67-5-1601, Tennessee Code Annotated requires assessors to perform a reappraisal over a four-, five-, or six-year period; however, reappraisal is not the sole responsibility of the office. This deficiency was in part attributable to the failure of management to accurately identify and post expenditures within the general ledger. RECOMMENDATION Officials should ensure that the general ledger accurately reflects transactions and account balances for the assessor’s office.

RECOMMENDATION: Officials should ensure that the general ledger accurately reflects transactions and account balances for the assessor’s office.

MANAGEMENT RESPONSE – DIRECTOR OF FINANCE: We do not concur with this finding. All positions in the county property assessor’s office contribute to reappraisal. The county is on a four-year reappraisal cycle and bills the cities in compliance with Section 67-5 1601(b)(2) Tennessee Code Annotated (TCA). Additionally, this TCA code does not specify a budget function. The assessor’s office works on a continuing basis to complete the reappraisal within the required four-year period. For example, they reappraise a certain percentage of parcels every year, to meet the four-year cycle. We have asked the auditors for examples of positions in the assessor’s office that do not perform the duties or support the reappraisals but received no examples. Our budget has been budgeted the same way for at least the last three years and our budget was approved by the comptroller’s office. We strongly believe the general ledger reflects the true nature of the transactions. Also, there are several counties in TN that currently utilize a single function budget for the property assessor’s office. We believe the sole purpose of the office is to appraise and reappraise property. Additionally, our reappraisal plan has been approved by the state board of equalization and is in compliance with the TCA mentioned above.

AUDITOR’S COMMENT: Assessors have existed in some form in Tennessee since at least the early 1800s. Their roles and responsibilities have evolved over time, but their core functions of identifying assessable property, tracking ownership, and making an assessment on such property existed long before the concept of mandatory reappraisal began around 1980. Based on this fact alone, it’s clear that certain functions must be performed regardless of whether properties are periodically revalued at current market value (reappraised). There are many duties and functions within an assessor’s office that are not directly related to the periodic reappraisal of real property. Furthermore, most counties in Tennessee do indeed account for operations of the Assessor’s Office and Reappraisal program separate on the accounting records. Therefore, management should maintain accounting and payroll records which separate reappraisal expenditures from the other expenditures of the assessor’s office.

FINDING Number 2: THE ASSESSOR DID NOT PROPERLY PRORATE IMPROVEMENTS AND NEW CONSTRUCTION - (Noncompliance Under Government Auditing Standards) Page 344:

The assessor did not properly prorate improvements and new construction. During the initial review of the operations of the assessor’s office by the Comptroller’s Division of Property Assessments it was determined that 106 single family dwellings had not been properly added or prorated for the 2023 tax year due to the assessor’s office failing to send change orders in a timely manner. A further review of building permits identified an additional 15 of the 95 items tested which had proration issues. Assessors are required to pick up new construction and improvements and to prorate their values for the portion of the year following their date of completion. Section 67-5-603(b)(1), Tennessee Code Annotated, provides that for the year in which an improvement or building is completed, the assessment, or increase in assessment, shall be prorated for the portion of the year following the date of its completion. This deficiency can be attributed to management’s failure to properly comply with this statute and resulted in an incorrect assessed value on the affected properties.

RECOMMENDATION: The assessor should properly prorate new construction and improvements as required by state statute.

FINDING Number 3: THE ASSESSOR DID NOT PROPERLY PICK UP ALL IMPROVEMENTS IN THE APPROPRIATE TAX YEAR - (Noncompliance Under Government Auditing Standards) Page 344:

The assessor did not properly pick up all improvements, specifically additions and outbuildings (objective data collection) discovered in the current review cycle. Instead, it was the practice of the office to defer what they deemed as “nominal changes” on the tax roll until the next reappraisal year of 2026. Section 67-5-1601 (b)(4), Tennessee Code Annotated, provides that where the on-site review is undertaken by the county assessor of property and the county assessor’s staff or a professional firm is employed to carry out this work, the division shall monitor the on-site review conducted by the county or the professional firm. This deficiency can be attributed to management’s failure to properly comply with this statute and resulted in an incorrect assessed value on the affected properties.

RECOMMENDATION: The assessor should put all improvements/objective changes in the appropriate tax year as required by state statute. The county should not be pushing objective changes to reappraisal tax years.

MANAGEMENT’S RESPONSE – ASSESSOR OF PROPERTY: We concur with the finding. We took immediate proactive action when it was brought to our attention. We discussed a series of reviews which would assist our office in finding anomalies.